The Balanced Scorecard

Summary

The Balanced Scorecard translates Mission and Vision Statements into a comprehensive set of objectives and performance measures

that can be quantified and appraised. These measures typically include several categories of performance such as financial

performance (such as revenues, earnings and return on capital) customer value performance (such as market share and customer

satisfaction measures), internal business process performance (such as productivity rates and quality measures), innovation

performance (such as percent of revenue from new products and rate of improvement index) and employee performance (such as

morale and best demonstrated practices)

Total Quality Management

Many of the Total Quality Management (tqm) concepts originated with the work of Dr. W. Edwards Deming, the American statistician.

During World War II he taught American industries how to use statistical methods to improve the quality of military

products. After World War II, General MacArthur took 200 scientists and specialists, including Dr. Deming, to Japan to help

rebuild the country. Many Japanese manufacturing companies adopted Dr. Demings philosophy.

Demings major philosophy is that quality improvement is achieved through the statistical control of processes and

the reduction in variability of these processes. Deming emphasises that management should encourage employee

participation and should encourage the employees to use their understanding of the processes and how they can be

improved (Munro-Faure and Munro-Faure, 1992, pp 291-292).

Dr. Joseph M. Juran broadened quality from its original statistical origin.

He stressed the importance of systems thinking that begins with product designs, prototype testing, proper equipment

operations, and accurate process feedback. Juran provided the move from Statistical Process Control to

Total Quality Control in Japan. This included company-wide activities and education in quality control,

and promotion of quality management principles. By 1968, Kaoru Ishikawa, had outlined the elements of Total

Quality Control management:

The Scorecard at Analog Devices, Inc.

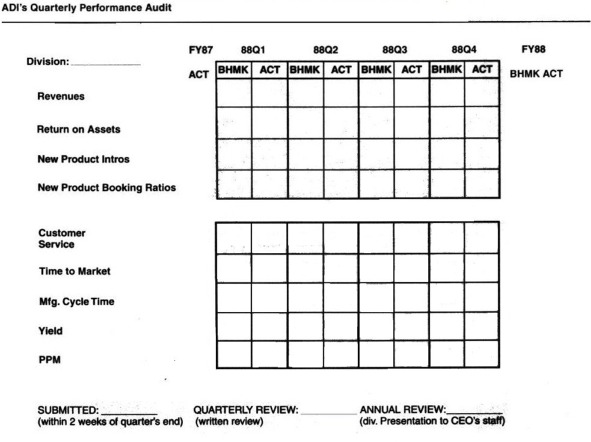

In 1986 Analog Devices, Inc. (ADI), a mid-sized semiconductor company, hired Art Schneiderman as Vice President

of Quality and Productivity Improvement. Schneiderman introduced goals for a series of quality measures that

correspond to what he considered to be the critical success factors for ADI (Anthony and Govindarajan, 1997).

As part of the five-year strategic plan of ADI, Schneiderman also developed a

one page report, called the Scorecard. This scorecard showed three categories of measures: financial,

new products and Quality Improvement Process:

The basic idea in creating this scorecard was to integrate financial and nonfinancial metrics into a single system in which they did not compete with one another for management airtime (Schneiderman, 2001).

The Balanced Scorecard in the 1990s

In 1990 Bob Kaplan invited Schneiderman to the Nolan-Norton study group on performance measurement. Bob Kaplan

and Schneidermann presented the use of the scorecard at Analog Devices, Inc. During

a second Nolan-Norton study the participants implemented scorecards within their organiations. Eric Norton,

who served as the project leader and facilitator, and Bob Kaplan wrote up the experiences of the participants

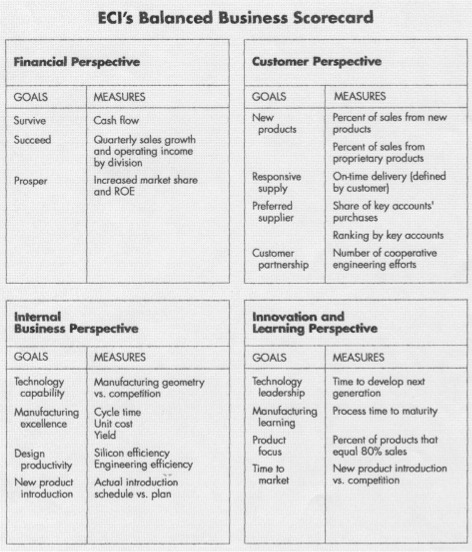

with the scorecard and devised a "balanced scorecard" in 1992. This balanced scorecard supplemented traditional

financial measures with criteria that measured performance from the perspective of customers, internal business

processes and innovation and learning. When using the balanced scorecard, companies articulate goals

for each perspective and translate these goals

into specific measures. An example (Kaplan and Norton, 1992):

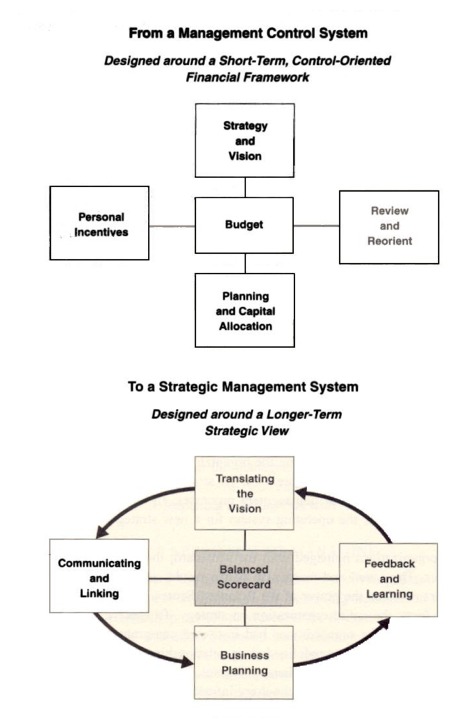

The Balanced Scorecard as a Strategic Management System

In 1996 Kaplan and Norton argued that the balanced scorecard could be used as a strategic management system which

supports four management processes (Kaplan and Norton, 1996):

- a higher customer satisfaction (a measure in the customer perspective) is correlated with

faster payments of invoices (a measure in the financial perspective) and faster payments result

in a higher return on capital (another measure in the financial perspective) or:

- improved information systems (a measure in the internal business processes perpective) result in

higher sales (measure in the financial perspective).

When a company implements the strategy it might found out that certain cause-and-effect relationships are not found

over time. In that case a company should reconsider the theory underlying the unit's strategy and might even

conclude that it needs a different strategy. This process of gathering feedback, testing the hypotheses on

which strategy was based and making the necessary adjustments is called "strategic learning".

BIBLIOGRAPHY

- Anthony, R. N. and V. Govindarajan, "Management Control System, 9th Ed.," McGraw-Hill Professional Publishing, January 1997, Case 11-1.

- Ishikawa, Kaoru. 'What Is Total Quality Control? The Japanese Way.' Englewood Cliffs, NJ: Prentice-Hall, 1985.

- Kaplan, R. S., D. P. Norton, 'The Balanced Scorecard - Measures that Drive Performance', Harvard Business Review, January - February 1992.

- Kaplan, R. S. and D. P. Norton, 'Using the Balanced Scorecard as a Strategic Management System', Harvard Business Review, January - February 1996.

- Kaplan, R. S. and D. P. Norton, 'The Strategy Focused Organization', Harvard Business School Press, 2001.

- Munro-Faure and L., M. Munro-Faure, 'Implementing Total Quality Management', The Free Press, 1992.

- Schneiderman, A. 'The first Balanced Scorecard: Analog Devices, 1986-1988, Journal of Cost Management, September/October 2001.